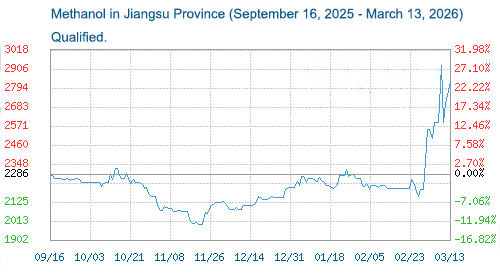

From March 6th to 13th (as of 15:00), domestic methanol prices at East China ports rose 9.15% during the period, a 28.65% increase compared to the previous week, and a 7.77% increase year-on-year. Domestic methanol market transactions remain primarily influenced by geopolitical factors, with rising sentiment in the futures market gradually transmitting to the spot market. Coupled with continued destocking by enterprises, localized external procurement of olefins to meet immediate needs, and the gradual recovery of downstream demand, methanol prices experienced a significant jump.

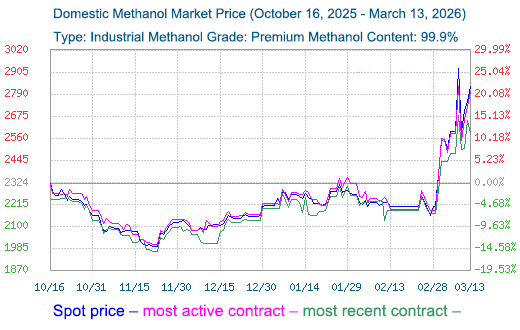

Methanol spot price comparison chart:

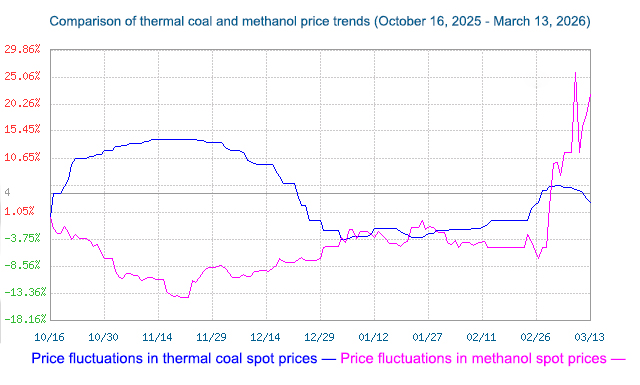

On the cost side, downstream coal enterprises are gradually resuming work and production, and demand is expected to increase, resulting in relatively stable market prices. The impact of costs is mixed.

Comparison chart of coal/thermal coal (upstream raw material) and methanol price trends:

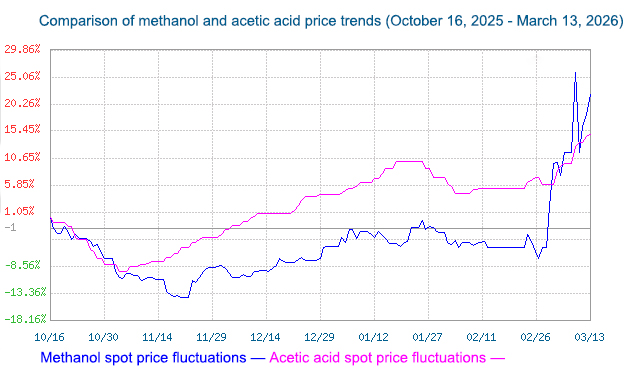

On the demand side, downstream sectors have been impacted by the surge in raw material methanol prices, leading to price increases for various downstream products. Currently, profitability is quite attractive, with MTO, glacial acetic acid, and methane chloride industries showing the most significant profit increases. Most downstream products are affected by methanol prices, resulting in a generally positive demand environment for methanol.

Price trend comparison chart of methanol and acetic acid (downstream products):

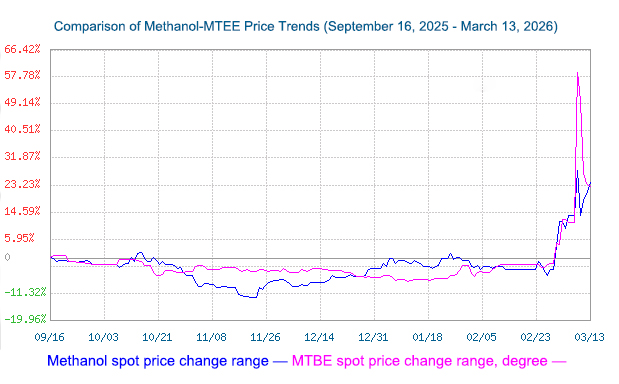

Comparison chart of methanol-MTBE (downstream products) price trends:

On the supply side, the maintenance of Zhongmei’s methanol plant was extended; Guangju New Materials and Inner Mongolia Black Cat’s plants resumed operations; overall losses exceeded recovery, resulting in reduced output and lower capacity utilization. Recently, the number of methanol plants scheduled to resume operations has increased, while the number of plants undergoing maintenance or reducing production has decreased, thus the overall market supply may increase. These factors are generally bearish for methanol supply.

On the international market, as of the close of trading on March 12, the CFR Southeast Asia methanol market closed at $494-496/ton, up $39.5/ton. The FOB US Gulf methanol market closed at 106-108 cents/gallon, up 2 cents/gallon; and the European FOB Rotterdam methanol market closed at €380-382/ton, up €13/ton.

Market outlook is foreseeable, with imports expected to decrease in the near term and upstream inventory reduction showing some activity, but the overall destocking effort is weaker than anticipated. Overall, the domestic methanol spot market is expected to consolidate with a slightly bullish bias.

Post time: Mar-16-2026