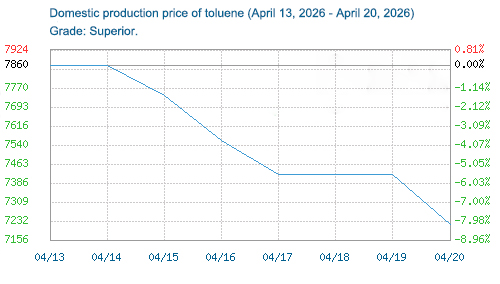

From April 13th to 20th, 2026, the domestic toluene market experienced a continuous downward trend, with prices in Shandong province falling sharply. The price of toluene in Shandong fell by 9.3% during this period. This was mainly due to a combination of factors, including weakening crude oil prices, relatively ample supply, and weak demand, which dragged down the market and resulted in a sluggish trading atmosphere and a cautious sentiment among market participants.

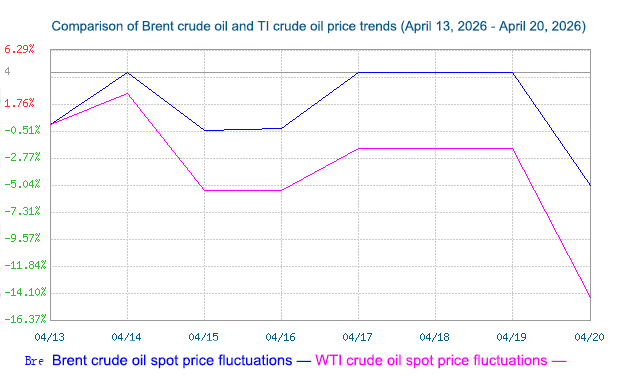

On the cost side: International crude oil prices initially declined before rebounding this week, with an overall downward trend, further weakening cost support for toluene. The volatile geopolitical situation in the Middle East caused significant fluctuations in crude oil futures prices. Although there was a brief rebound after the initial sharp decline, it failed to provide sustained support. The pullback in crude oil prices directly weakened support for toluene production costs. Coupled with increased market concerns about the future trend of crude oil prices, the transmission of positive cost-side factors was hindered. Meanwhile, the price spread between benzene and toluene remained wide, and the arbitrage window between PX and mixed xylenes opened, providing some support for toluene, but the strength was limited and insufficient to offset the negative impact of weakening crude oil prices.

Brent-WTI crude oil price comparison chart:

Supply Side:

The domestic toluene market supply remained ample, with major refineries and Shandong local refineries actively shipping their products, resulting in sufficient market supply. This week, major domestic refineries such as Sinopec and PetroChina maintained stable operation of their toluene units, lowering their listed prices in line with market conditions. In South China, companies like Guangzhou Petrochemical, Maoming Petrochemical, and Sinopec Refining & Chemical maintained stable sales. In Shandong, local refineries maintained high operating rates, and influenced by the continued decline in market prices, refineries were more willing to ship, actively lowering prices to increase sales volume. Although the second quarter is traditionally the industry’s maintenance season, with companies like Jinling Petrochemical and Taizhou Petrochemical having maintenance plans, no large-scale maintenance was implemented this week, resulting in sufficient overall domestic toluene capacity. Coupled with reasonable inventory levels at East China ports, the market had ample supply, significantly suppressing prices from the supply side.

Demand Side:

Downstream demand for toluene remained weak, with insufficient support from essential demand. During the week, downstream industries such as TDI, coatings, and solvents maintained low operating rates, resulting in sluggish end-market consumption. Downstream factories primarily adopted a just-in-time purchasing strategy and maintained low inventory levels, showing significant resistance to high toluene prices. Even with consecutive and substantial price reductions, downstream restocking remained slow, with most transactions consisting of small, essential orders and few large transactions. Demand was insufficient to provide effective support for the toluene market.

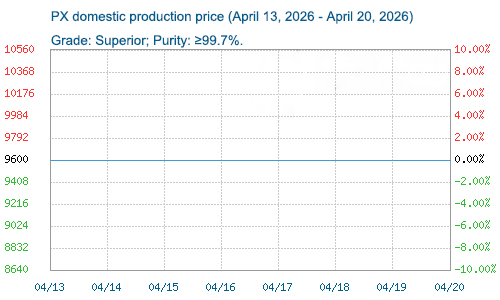

PX price trend chart:

Market Outlook:

In the short term, the domestic toluene market will continue to face multiple pressures and is likely to maintain a weak and volatile trend. On the cost side, the trend of crude oil prices remains uncertain; if crude oil continues to weaken, it will further drag down toluene prices. On the supply side, the loose supply situation is unlikely to improve significantly in the short term, and ample market supply will limit the potential for price rebounds. On the demand side, the recovery of downstream industries is slow, and the release of pent-up demand is limited; the follow-up of procurement will be a key variable in the market. It is expected that the toluene market will not see a significant reversal in the short term. Going forward, close attention should be paid to crude oil price fluctuations, the pace of restocking by downstream factories, and changes in market news, and vigilance should be exercised regarding the risk of further price declines.

Post time: Apr-22-2026