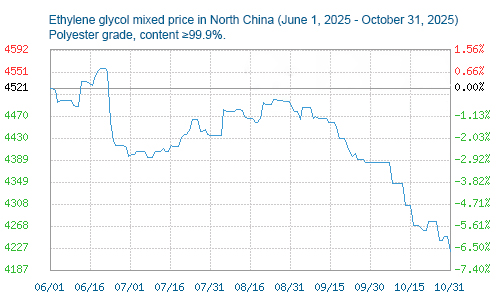

Ethylene glycol prices shifted downward in October.

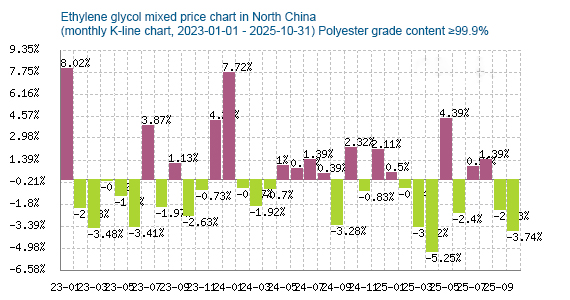

Ethylene glycol prices continued to fall in October, with the price center shifting downwards. As of October 31, the average price of domestic oil-based ethylene glycol was 4220.83 yuan/ton, a decrease of 3.74% compared to the average price of 4385 yuan/ton on October 1.

Regarding ethylene glycol at ports, the basis for spot ethylene glycol contracts (minimum 500 tons) was affected by the delivery factor at the Yangtze River International Warehouse, leading to weakened market trading sentiment. However, some companies showed strong interest in their existing spot inventory, resulting in a near-term stronger and far-term weaker basis. This week’s contract basis trading range was +84 to +88; by the close of trading, the basis for next week’s contract was quoted at +75 to +77, and the basis for the November contract was quoted at +72 to +74.

The domestic spot price for coal-based polyester grade ethylene glycol (bulk, including tax, self-pickup) for full-order truck delivery was 3770-3880 yuan/ton.

The main reasons for the decline in ethylene glycol prices in October:

The decline in ethylene glycol prices in October 2025 was the result of a combination of factors, primarily including increased supply, weak demand, and the macroeconomic environment, as detailed below:

Supply side

Domestic capacity continues to expand: China’s total ethylene glycol production capacity is projected to exceed 28 million tons by 2025. This rapid growth in domestic capacity has led to a significant increase in supply, intensified market competition, and gradually revealed the pressure of oversupply, pushing prices downward.

High plant operating rates: Domestic ethylene glycol plants are operating at high rates, with the total domestic load reaching 77% in October, of which the syngas-based plant load reached 81.89%, ensuring ample market supply.

Increased imports: Imports in October are estimated at 650,000 tons. The concentrated arrival of overseas goods further increases the supply pressure in the domestic market.

Demand side

Downstream polyester demand growth fell short of expectations: The main downstream industry for ethylene glycol is the polyester industry. Although some polyester plants have restarted, overall demand growth has been limited. Orders from the weaving sector are relatively weak, and inventories of filament and staple fiber products have accumulated, leading to weak demand for ethylene glycol from polyester plants.

Weak end-user stockpiling: Downstream end-user companies are cautious about market expectations and have weak stockpiling intentions, making it difficult to effectively release market demand and providing strong support for prices.

Cost-related factors: The continued decline in crude oil prices has significantly narrowed the losses of integrated naphtha-based ethylene glycol production, weakening cost support and putting downward pressure on ethylene glycol prices.

November Ethylene Glycol Market Outlook

Yulong Petrochemical’s new 800,000-ton unit went into operation in September, and Ningxia Changyi and other capacity units are scheduled to start trial operations in the fourth quarter. This new capacity is expected to put pressure on supply, while there is limited capacity undergoing maintenance, resulting in significant overall supply pressure. The polyester industry is currently operating at a high rate, and with the peak season nearing its end, downstream weaving demand is expected to weaken, leading to a potentially weaker demand outlook.

Ethylene glycol port inventories remain relatively low. Prices have fallen significantly and recently showed signs of stabilizing. The market outlook is awaiting the strength of bullish support. Ethylene glycol prices are expected to bottom out and rebound in November, with a high probability of an initial weakness followed by a stronger trend.

Post time: Nov-03-2025