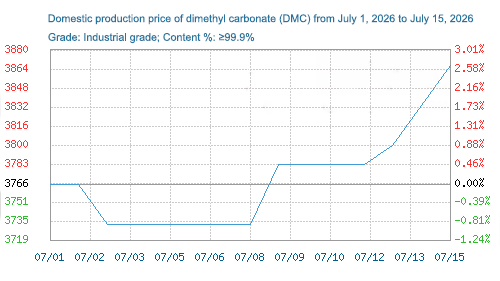

In the first half of July, the industrial-grade dimethyl carbonate market showed a slight, steady increase with narrow-range, slightly stronger fluctuations. In the middle of the month, supported by rising raw material costs and tight spot supply due to maintenance at some plants, market prices rose slightly, and the transaction focus slowly shifted upward. However, weak end-user demand limited the price increase, and no sustained upward trend emerged. As of July 15, the average price of domestic industrial-grade dimethyl carbonate had increased by 2.65% compared to the beginning of the month.

Cost side: Rising raw material prices provide rigid support

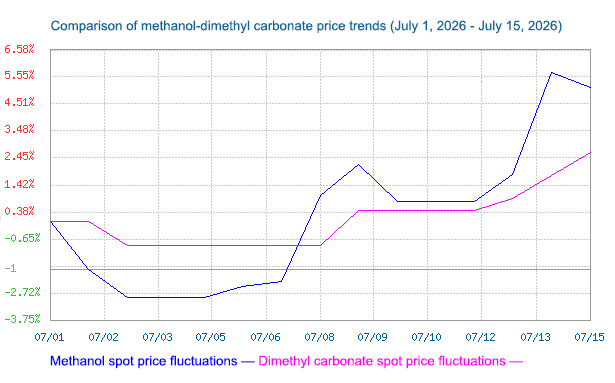

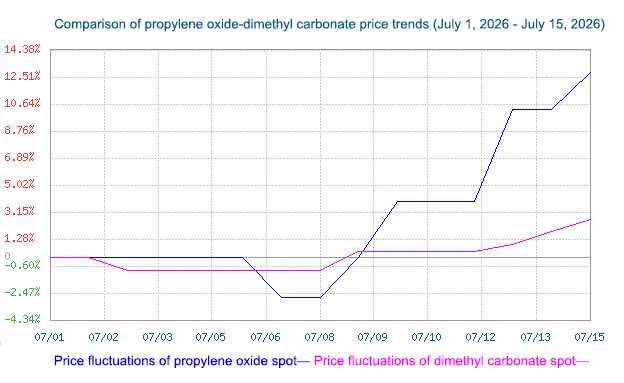

In the first half of July, the markets for methanol and propylene oxide, upstream raw materials for dimethyl carbonate, saw significant price increases, shifting the overall cost of raw materials upward and providing sustained and rigid support for the dimethyl carbonate market. Increased production costs for manufacturers, coupled with compressed profit margins across the industry, led to a weak willingness among producers to sell at low prices. Consequently, they generally maintained high prices and were reluctant to sell, effectively supporting dimethyl carbonate market prices and curbing the risk of a downward trend.

Supply side: Spot supply is tight, and the pace of supply increase is slow.

In early July, many domestic dimethyl carbonate (DMC) plants undergoing maintenance had not yet resumed operation, and the overall operating rate of the industry remained at a low to medium level. Total spot inventory was low, and the tight spot market provided strong support for prices. By mid-July, some previously shut-down plants gradually restarted, leading to a slight increase in spot supply. However, the pace of plant restarts was slow, limiting the short-term increase in supply and failing to quickly alleviate the tight spot market situation. Meanwhile, major producers had no inventory pressure, and the overall supply pace was stable, with no instances of large-scale dumping. The overall supply side remained favorable, but the strength of this positive factor gradually weakened.

Demand side: Essential needs provide a safety net, but incremental growth is severely insufficient.

Overall, weak demand is the core factor limiting a significant price increase. Demand diverges significantly across the two main downstream sectors: demand in the lithium battery electrolyte sector remains relatively stable, with the new energy industry maintaining steady inventory levels and continuing routine, essential purchases, providing basic support to the market; while traditional downstream industries such as polycarbonate (PC), coatings, and adhesives are in their traditional off-season, with insufficient capacity utilization and a generally weak industry trend. Companies are exhibiting low purchasing enthusiasm, primarily relying on just-in-time purchases and small-scale replenishment, without concentrated or large-scale inventory buildup.

Market Outlook:

In late July, the domestic dimethyl carbonate (DMC) market is expected to continue its narrow-range, slightly bullish trend. Overall, the upward momentum will slow, with limited upside potential and no risk of a significant drop. The market is likely to maintain a stable, stagnant pattern. The core fluctuation range is limited, with insufficient momentum for either upward or downward movement, resulting in a generally stable market with minor fluctuations.

Post time: Jul-16-2026