During this period (September 19 to 25, 2025), acrylic acid and butyl acrylate prices generally showed a mixed trend of increases and decreases. Capacity utilization rates for acrylic acid and butyl acrylate decreased slightly during the week, pushing up bids from holders. Early in the week, driven by expectations of rising prices and demand for restocking, both buyers and sellers were enthusiastic and trading sentiment was positive. However, mid-week, downstream companies showed less acceptance of high prices, adopting a cautious purchasing strategy. Market competition intensified, leading to a somewhat stagnant trading atmosphere.

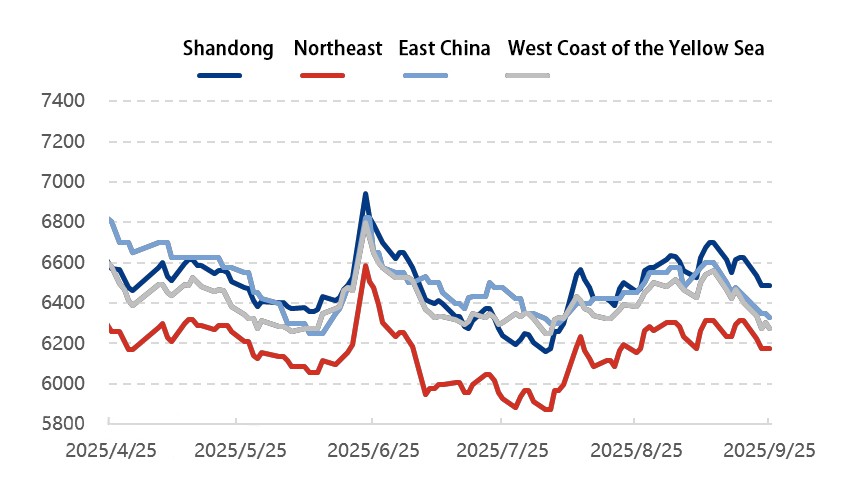

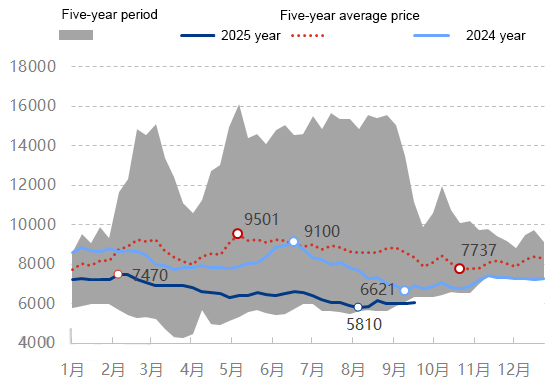

The acrylic acid market saw a volatile upward trend this period, with capacity utilization declining compared to the previous period. Comprehensively measured supply-side data showed a decline. This week, Shandong Hongxin and CNOOC units underwent maintenance, resulting in a slight decrease in on-site supply and a decrease in capacity utilization. Factories and holders maintained firm quotes, while downstream users responded with strong demand, leading to robust market negotiations. Butyl acrylate capacity utilization decreased compared to the previous period, with factories and holders offering flexible quotes. Downstream users maintained a wait-and-see attitude, resulting in quiet trading on the market, with some strong demand following suit.

The next cycle forecast indicates that acrylic acid and butyl acrylate capacity utilization rates are expected to remain stable, with a generally neutral market trading atmosphere. Holders are trading according to market trends, with actual transactions focused on negotiation and downstream inquiries based on demand, resulting in a stagnant trading atmosphere. Based on supply and demand fundamentals calculated based on the start-up and shutdown status of upstream and downstream plants, acrylic acid prices are expected to fluctuate within a range, while butyl acrylate prices are expected to consolidate.

Raw material analysis

During this period (September 19 to 25, 2025), domestic propylene market prices declined this week. Increased supply and weak demand were the primary factors driving the downward shift in the price center of gravity. The main bearish factor for the propylene market this week was the increased supply brought on by the commissioning of a cracker on the Shandong coast. News of the pending restart of a PDH facility in Dongying further deepened bearish sentiment among industry players, leading to a continued decline in propylene prices. Furthermore, continued PP plant shutdowns due to cost pressures contributed to weak demand, putting pressure on spot propylene prices in both the northern and southern markets. As of now, there has been no significant price differential between propylene monomer and PP, failing to attract active downstream buying, leaving propylene prices with further room to fall. As of September 25, the mainstream transaction price of propylene in Shandong was 6,485 yuan/ton, a 2.11% decrease from the previous week; the mainstream transaction price of propylene in East China was 6,330 yuan/ton, a 1.94% decrease from the previous week.

The domestic n-butanol market remained strong this week after a surge, with overall trading sentiment improving over the weekend. Production plants have been operating steadily this week, keeping inventories low, and some major plants fulfilling pre-sale orders. Consequently, spot n-butanol supply is limited. With the approaching holiday season, downstream buyers are actively seeking bargains. Furthermore, increased production capacity at downstream butyl acetate plants is leading to a slight increase in demand, increasing market inquiries and transactions, and consequently, a slight price increase. As the weekend approaches, following a round of centralized procurement, downstream users are becoming cautious about chasing higher raw material prices, resulting in limited transactions at high prices. n-butanol plant inventories remained low before the holiday, with orders remaining in pre-sale order books, and the market sentiment towards high prices has cooled slightly.

Related product market analysis

Isooctyl acrylate: The domestic isooctyl acrylate market remained strong this cycle, with raw material octanol consolidating at a low level. Costs remained stable, with manufacturers and holders actively supporting the market and maintaining high quotes. End users entered the market and purchased as needed, with firm order negotiations fluctuating at a high level. As of the afternoon close of September 25, the price of isooctyl acrylate was 9,450 yuan/ton, a month-on-month increase of 5.48%.

Methyl acrylate: The methyl acrylate market saw a downward trend this week. Factories and holders quoted prices based on market conditions, creating a wait-and-see atmosphere within the market. Some downstream users were just following through on demand, resulting in limited actual trading. Market negotiations focused on a period of fluctuating declines and consolidation. As of the afternoon close of September 25th, the price of methyl acrylate was 7,700 yuan/ton, down 1.75% month-on-month.

Ethyl acrylate: This week, the ethyl acrylate market maintained a stable operation. Ethyl acrylate factories and holders quoted prices according to market conditions. Downstream users mainly digested contracts or inventories, and some users with urgent needs followed up with inquiries to replenish stocks. The negotiation focus range was stable.

Post time: Oct-09-2025