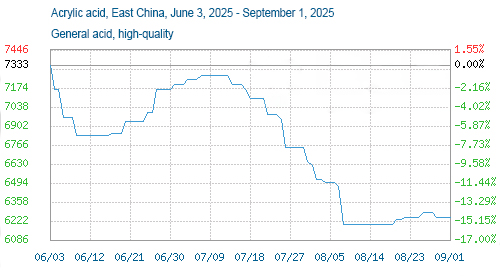

Entering September 2025, acrylic acid market prices continued to be under pressure. As of September 1, the benchmark price of acrylic acid had fallen by 6.02% compared to the beginning of the previous month. This was primarily due to continued weak demand and a strong wait-and-see attitude among downstream buyers, who only purchased for essential needs and showed little interest in stockpiling large quantities of goods.

The current market downturn is the result of multiple factors on both the supply and demand sides:

1. Continued supply pressure: In the second half of 2025, the domestic acrylic acid industry still has plans to commission over 600,000 tons, or even 740,000 tons, of new production capacity (e.g., at Shandong Blue Bay and Tianjin Bohai Chemical). This has further intensified supply pressure in the industry. Although the industry’s operating rate remains at a low-to-medium level of around 68%, attempting to balance supply and demand through load reduction, social inventories remain moderately high, and inventory pressure persists.

2. Weak demand: Downstream key sectors (such as coatings, adhesives, and textile auxiliaries) are showing limited purchasing enthusiasm, generally adopting a bearish or cautious approach, focusing primarily on replenishing inventory to meet demand, and engaging in widespread price-cutting. The export market is also bleak. In the first half of 2025, China’s butyl acrylate exports decreased by 13.42% year-on-year, failing to effectively alleviate domestic supply pressures. Traditional demand sectors (such as oil extraction, water treatment, and papermaking) are hampered by the global economic downturn and are unlikely to see significant growth.

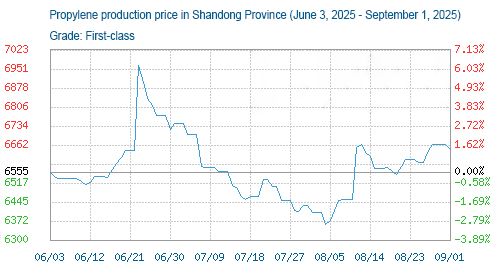

3. Cost Support and Game of Thresholds: While the price of propylene, the primary raw material, has risen since early August, the benchmark price for propylene on Sinochem was 6,663.25 yuan/ton on September 1st, a 3.58% increase from 6,433.25 yuan/ton at the beginning of the previous month. At current prices, some factories are nearing break-even or even operating at a loss. Consequently, manufacturers have limited room for profit concessions and are strongly motivated to maintain prices. The market is locked in a fierce battle between cost support and weak demand.

Future Outlook

In the short term, the acrylic acid market will continue to consolidate at a low level, with limited upside and downside potential. Unless there is an unexpected improvement on the demand side (such as centralized procurement by large downstream companies or a surge in export orders) or a significant increase in the cost side (propylene), sustained price increases are unlikely. If propylene prices plummet or downstream demand remains sluggish, high inventories and weak demand will continue to weigh on the market.

In the medium to long term, the acrylic acid industry is undergoing a transition from “scale competition” to an “era of technology premium.” Leading companies (such as Satellite Chemical and Huayi Group) are building barriers through technological iteration and industry chain integration, while small and medium-sized enterprises, due to insufficient technological investment, struggle to meet high-end demand (such as medical-grade and electronic-grade acrylic acid), increasing their survival pressure.

In summary, the core characteristic of the current market is the fierce competition between “weak demand” and “high costs,” resulting in a price dilemma, a downward shift in the overall center of gravity, and a generally wait-and-see attitude among market participants.

Post time: Sep-01-2025